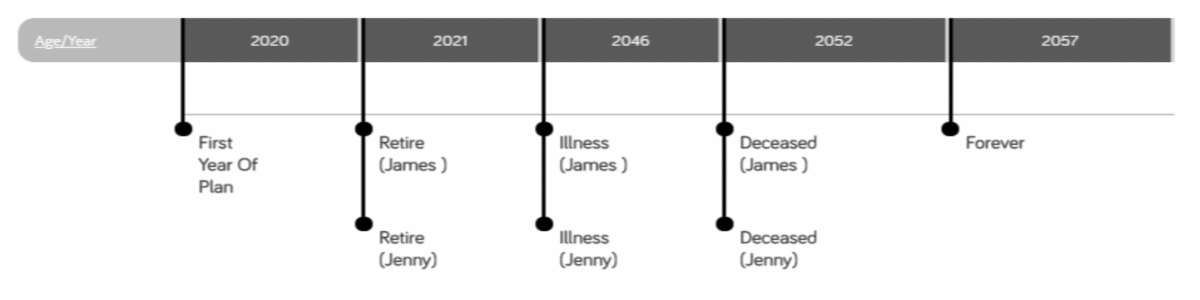

BESPOKE PLANNING

We helped James and Jenny visualise their financial future and assess sustainability:

ANALYSIS

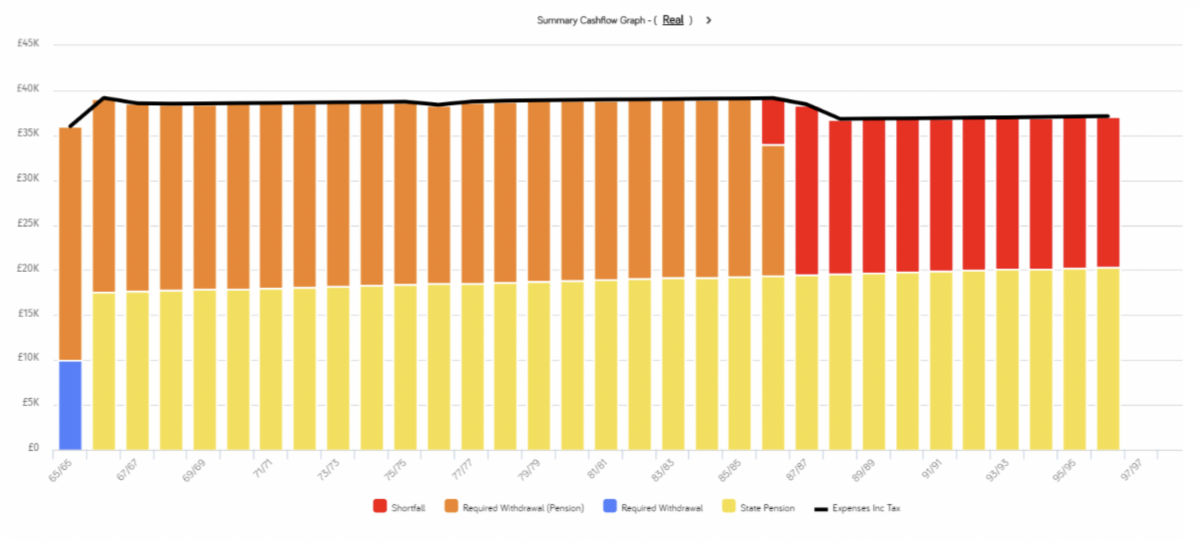

Our analysis, based on agreed assumptions with no downsizing event, indicated that James and Jenny would be unlikely to support their desired lifestyle in retirement. Our analysis indicated that their savings and personal pensions would likely be exhausted in their late 80.

RESULTS

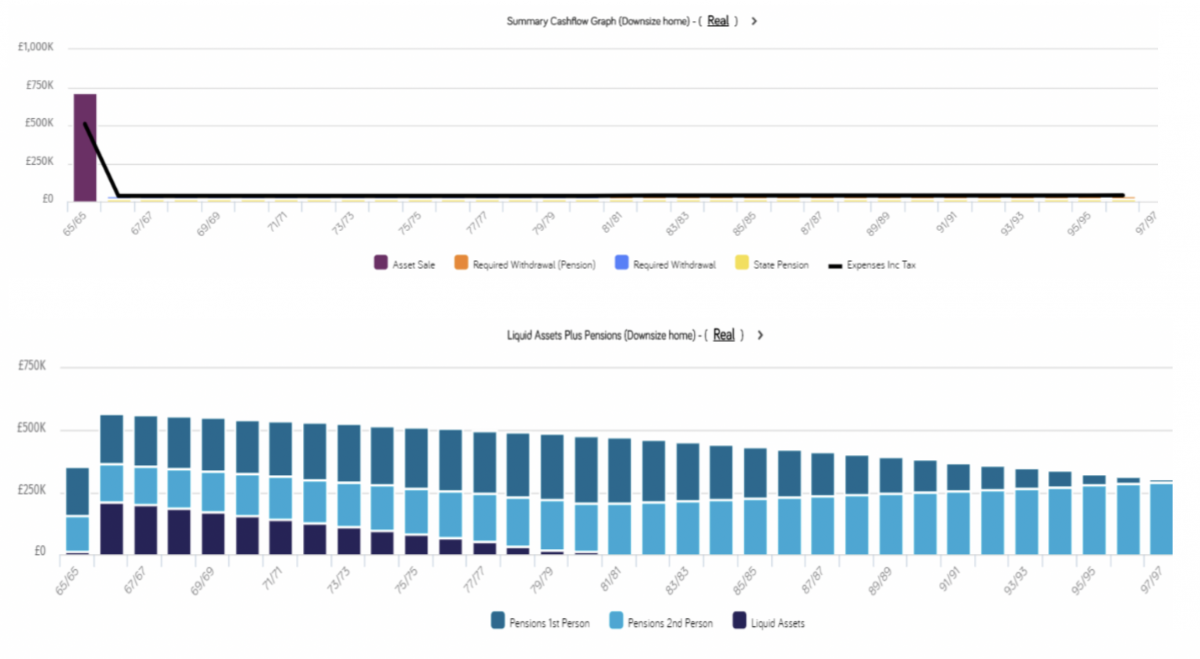

We showed James and Jenny how downsizing in 12 months’ time could improve the chances of them sustaining their desired lifestyle in retirement.