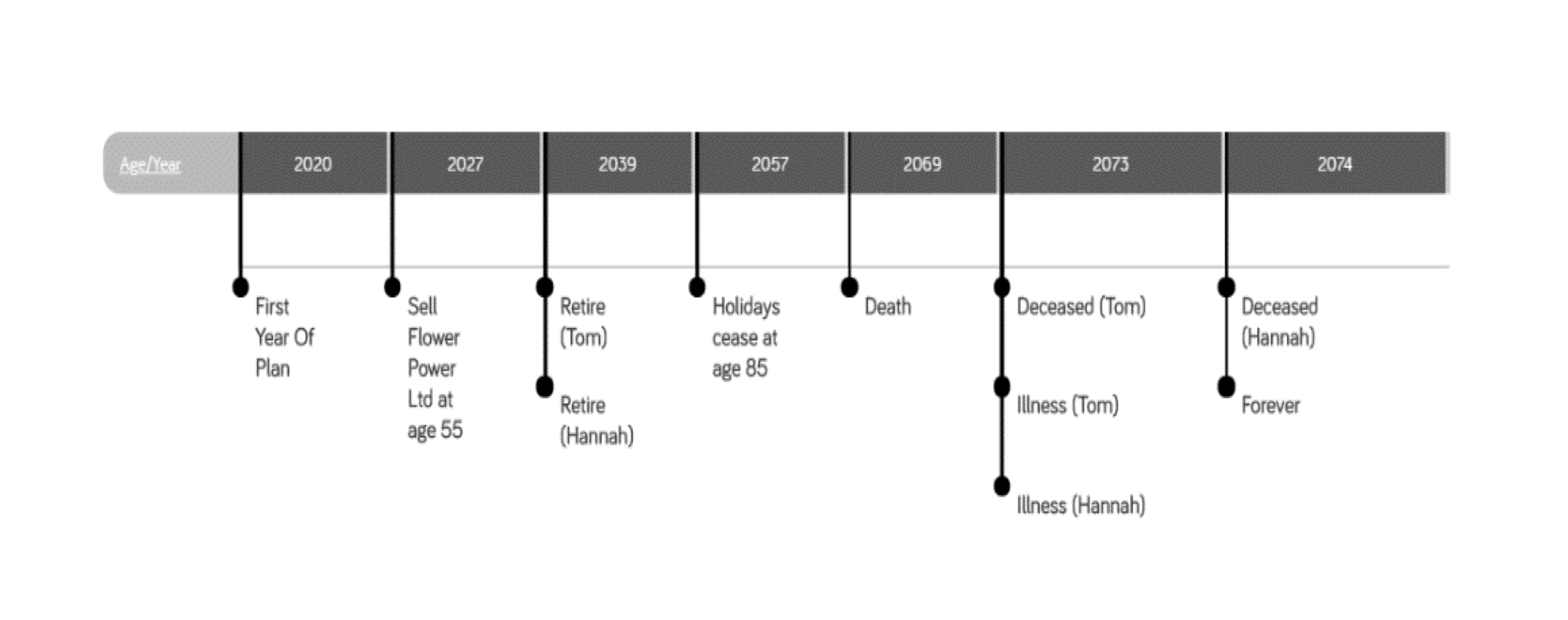

SYNTHESIS BESPOKE FINANCIAL PLAN

We helped Hannah and Tom visualise their current financial future:

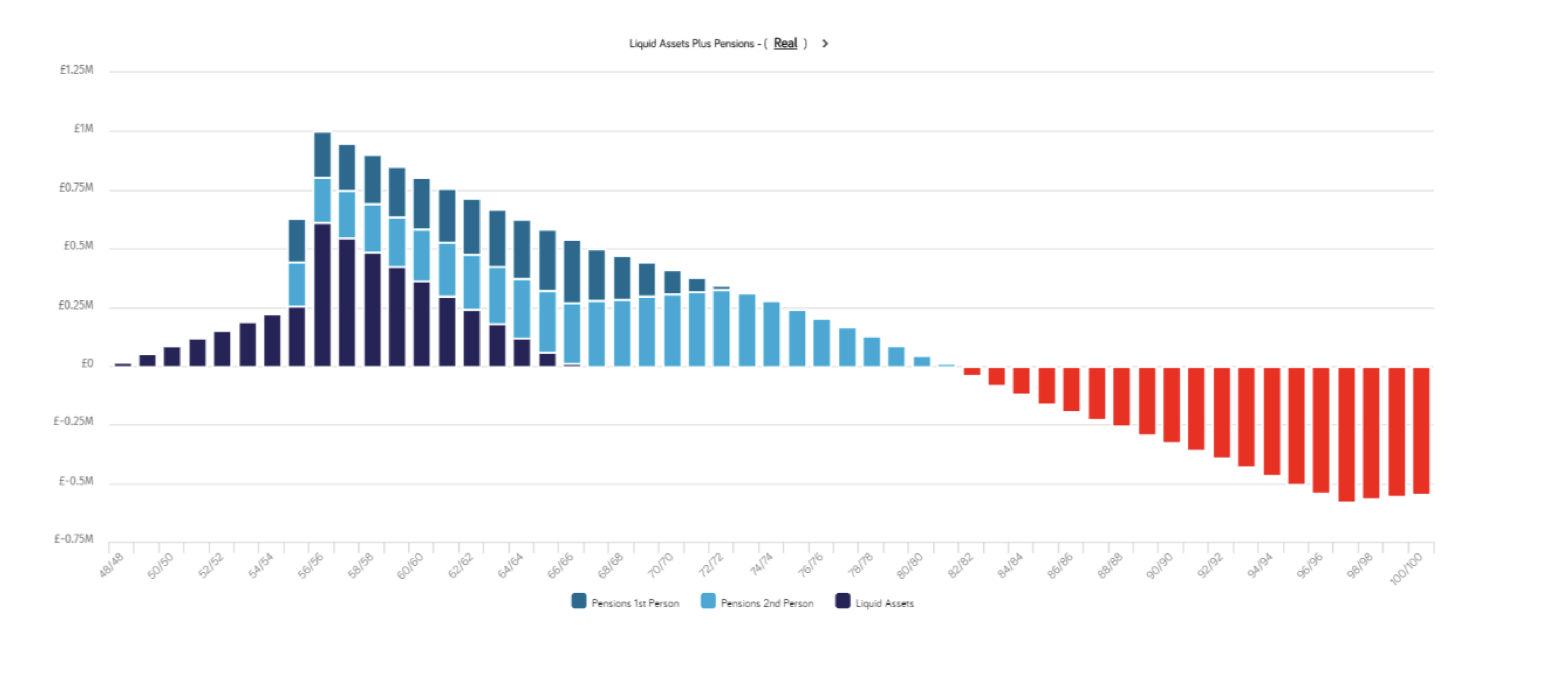

ANALYSIS

Based on our agreed assumptions, our analysis indicated that Hannah and Tom would be unlikely to support their desired lifestyles in retirement.

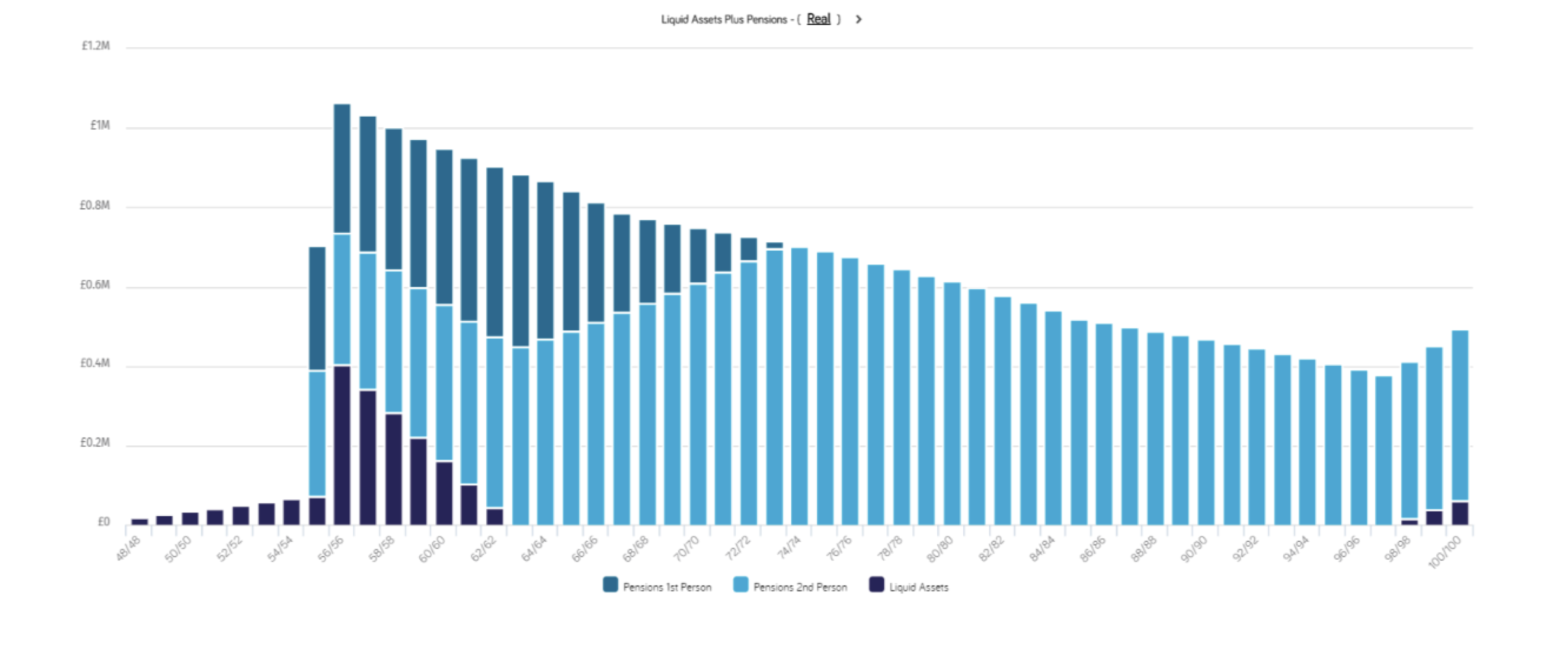

RESULTS

We showed Hannah and Tom how they could improve the chances of sustaining their desired lifestyles in retirement by making some key strategic changes today. This included making additional employer pension contributions and adjusting their investment strategy from today.